Fuel for Thought: Warning signs on the path to mass EV adoption

LISTEN TO A PODCAST ON THIS TOPIC WITH S&P GLOBAL MOBILITY EXPERTS

Just what you wanted: Yet another analysis regarding vehicle electrification. But bear with us; this one is necessary reading. Yes, the battery-electric vehicle (BEV) market is taking off, perhaps at a more rapid clip than some have predicted. But that does not mean the industry is home-free in transitioning from the internal combustion era to BEVs. Even if forecasted market demand crosses the chasm to mass adoption, there are several major impediments to BEVs becoming the de facto transportation propulsion technology. Those who do not take heed are destined to fail.

For all the fervor of early adopters predicting this transport transition as revolutionary as that of horses to cars, there's a certain fragility to the current BEV movement. The effort and cajoling required to bring fire to life — from demand- and supply-side incentives to technology-forcing regulation and legislation — is bound to be more susceptible to roadblocks compared to one evolving organically.

The equation of reaching mass-market adoption of electrified vehicles is as-yet unproven. And while certain markets — be it mainland China or San Francisco — are embracing a BEV future, inventories of BEVs in the US market are showing early signs of stacking up on dealership showroom floors. As such, it is still far from a realistic mass-market proposition. While BEVs achieving price parity with their internal combustion engine (ICE) counterparts will unlock the keys to the door marked "mass-market," there are still residual issues that need addressing other than achieving supply-and-demand equilibrium at mass-market volume. Numerous other movements in play must be implemented to ensure BEVs are not just a one-and-done phenomenon.

If successful, however, the electrification transition will upend the industry's infrastructure, economics, technologies and supporting services in a way that stakeholders are only just starting to address and comprehend. Some will be left holding the reins of a disappearing business just as owners of horse-drawn carriage companies experienced over 100 years ago.

The latest S&P Global Mobility forecast details the key facets of the electrification push that need careful monitoring to ensure the smoothest continuing transition for all stakeholders.

A warning about the supply chain

In the ICE era, the automotive sector became well-versed in dealing with supply chain risk. Now with electrification, the parameters have changed; risk is now presented further upstream from the sector's normal realms of operation.

Previous supply chain snarl-ups and surprises — such as the Xirallic pigment shortage from the Japan earthquake/tsunami in 2011, and the pandemic-triggered semiconductor crisis — will seem diminutive in comparison. These disruptions prompted increased focus on supply chain visibility, but in the electrification era, the reliance on certain raw materials and parts could present its own set of challenges on a routine basis.

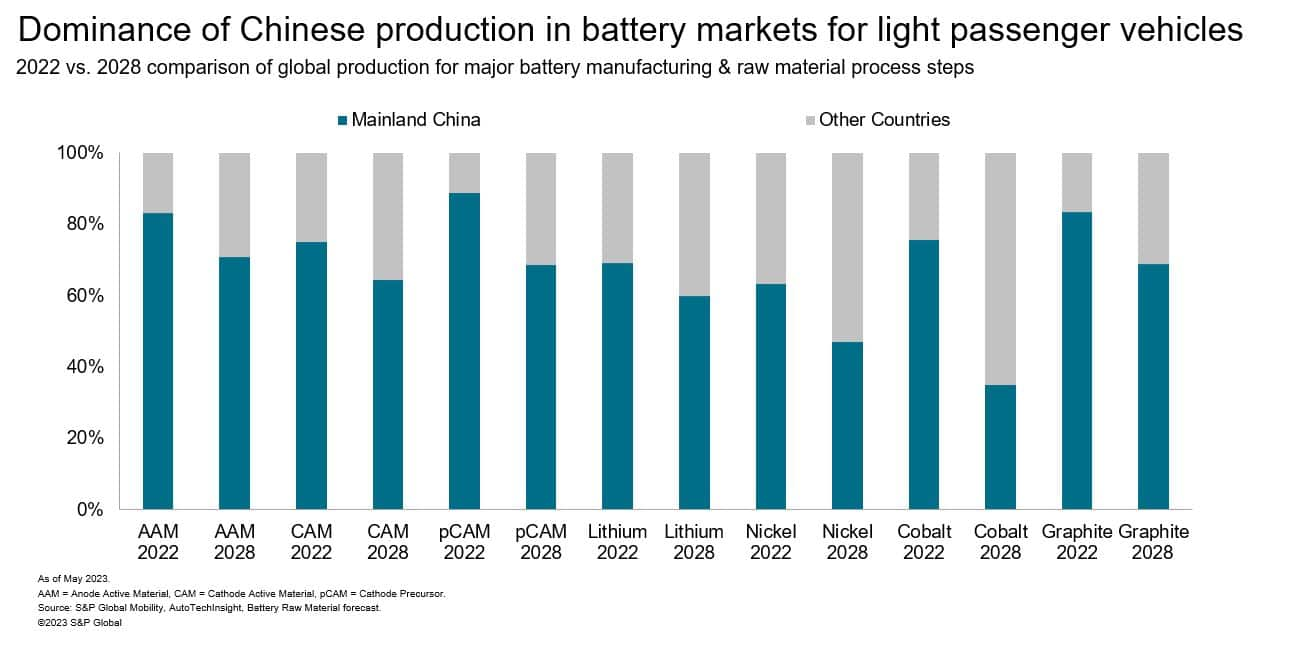

Efforts by mainland China's auto industry to establish a first-mover position throughout the BEV supply chain have been successful. The main pieces of constructing the EV battery — the cathode and anode in the traction-battery cells and the pack itself — as well as significant stakes in inverters, converters, controllers and charging tech have been snapped up by the mainland Chinese supplier base. Meanwhile, laggard regions are planning to use legislative levers for a semblance of control and to catch up with mainland Chinese counterparts. We expect some of the gap to mainland China to be clawed back as the market expands and the diversity of battery chemistries continues.

However, those components are nothing without their raw materials, and mainland China also holds an advantage — either in accessing those elements locally or sourcing them from other countries via an aggressive trade policy. The following illustration highlights S&P Global Mobility's May 2023 forecast for key raw materials and their sourcing.

In the case of battery raw materials, a supply crunch could exist within this decade. For lithium, we forecast a sixfold increase in demand between 2022 and 2030 from some 0.06 million metric tons to 0.37 million metric tons for light passenger vehicle applications alone. Together with the S&P Global Commodity Insights team, we also expect lithium markets will be in deficit by 2027, creating a bottleneck for automotive supply. Resolution will be slow as lithium takes on average 15.7 years to reach the market after initial discovery. Hence the recent focus on battery recycling.

Other composite elements of the cathode — the most expensive part of the battery — dominate concerns around raw materials. Our forecast reflects the pursuit of increased energy density through more nickel-rich chemistry, coupled with a growing desire to limit its use to applications where the range is critical. Lithium iron phosphate-derived technology will be selected with increasing regularity in lower-cost applications.

However, in addition to lithium and nickel, cobalt is a key element in battery chemistry. Sourcing of cobalt — of which 75% of the world's current supply comes from the troubled Democratic Republic of Congo — presents a snag for any company trumpeting an ESG or sustainability ethos. Companies are looking for alternate ways to source elsewhere by the end of the decade — as well as to process this element, as mainland China dominates this link of the supply chain as well.

It is not only in battery raw materials that mainland China has established an eminent position. It enjoys a lofty position for the rare earth elements necessary for electric motors. This has recently been brought sharply into focus by mainland China's announcement that it wants to control exports of gallium and germanium, resulting in many outside countries quickly reassessing their supply chain exposure.

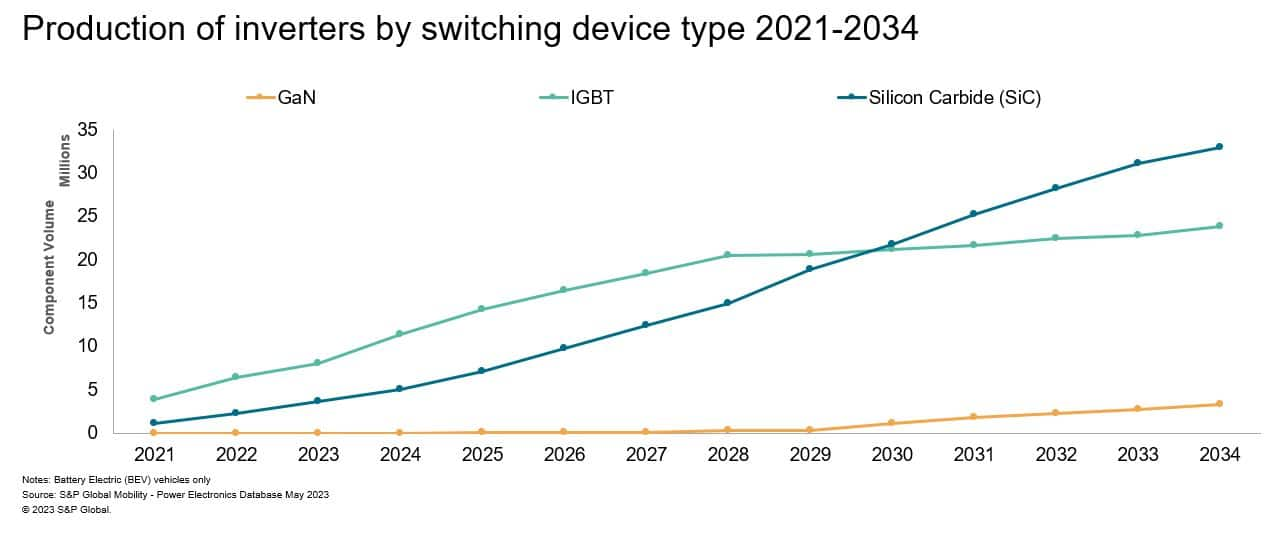

Gallium is a material necessary for certain power electronic components. Power electronics such as inverters, DC-DC converters and onboard chargers are being reworked to encompass more efficient designs using silicon carbide (SiC)-based chips, promising increased semiconductor demand and the accompanying supply challenges. The growth of silicon carbide-based inverters is shown in the following chart.

There are also the seemingly mundane metals, such as copper, which is already under significant pressure, and industry leaders are predicting a shortage by the end of the decade. Manganese might also be deemed abundant given its use in the steel industry, yet battery-grade quantities of the required electrolytic manganese dioxide (EMD) are in comparatively short supply, especially in free-trade agreement countries.

Amid this shift, automakers are developing in-house solutions to assert a degree of security over nascent supply chains. With such high stakes, relationships between OEMs and Tier 1s are inevitably strained.

As a consequence of the chip shortage, a richer portfolio mix has allowed OEMs to achieve higher margins across their product lines, giving headway to fund BEV transitions. For Tier 1s, there has been no such dividend. As BEVs are fundamentally simpler, in-house manufacture of the battery, propulsion system and power electronics will result in OEMs having responsibility for a much higher proportion of the vehicle's value — piling pressure on suppliers.

There is also the manufacturing side of the equation that relies on these component parts. Aside from actual BEV demand, battery capacity per vehicle is a growth vector — average capacity is forecast to increase from 60 kWh to 78 kWh — contributing to global demand during 2023-30 increasing from 540 GWh to 3.4 TWh.

Given this increase, battery-cell manufacturing capacity must increase in tandem. As a result, we expect the total theoretical manufacturing capacity (for light passenger vehicles) to increase from 1.35 TWh to 4.5 TWh by 2028, with the number of battery-cell manufacturing plants rising from 107 to 188 globally. If construction schedules are met, there will be sufficient capacity — indeed some underutilization will occur.

Who owns the propulsion technology?

OEMs traditionally are responsible for their engine and, in some cases, transmission requirements. But they now face off against Tier 1 powertrain suppliers to bring e-axles and their subcomponents in-house. For comparatively low volume first-generation BEVs, OEMs largely outsourced to Tier 1 specialists. Now they are bringing more of the integrated, three-in-one (motor, transmission, and inverter) e-Axles to their own facilities. Our latest data show over 75% of OEMs now perform the e-Axle integration activities in-house.

Regardless of who builds e-Axles, by 2025, 80% of eAxle-based motors will need the aforementioned rare earth elements germanium and gallium. As a result, we estimate that well over 90% of the world's production-ready magnets will be mainland Chinese-manufactured.

Opportunities for suppliers remain in the motor assembly, with 47% of motors produced in 2023 being outsourced. But as volumes increase, these supply chain opportunities will evolve as the motor will be broken into subcomponents like rotor and stator assemblies. Already Tier 1s are taking advantage of these opportunities. However, the e-Axle is a cautionary tale as to how an OEM's sourcing remit can change — while trying to keep their employment numbers steady during the transition.

A second issue for motors — garnering fewer headlines, but the subject of earlier S&P Global Mobility research — is the lack of thin-gauge electrical steel capacity required for assembly. Concerns persist, with more investment in electrical steel capacity needed to meet burgeoning demand.

There aren't enough chargers

Once the vehicles are built, then comes the "refueling" equation. The BEV paradigm opens the opportunity to recharge the vehicle in a multitude of domains aside from conventional public refueling infrastructure familiar to gasoline service stations. However, for now, public charging options are constrained by not just the quantity of chargers available but also the reliability of the stations, the delivery speed of electrical power, and the battery's ability to receive it.

There also is the relative first-world nature of BEV charging, as developing nations may not have the infrastructure grid to support a mass charging network. Therefore, much of the underdeveloped world will likely remain an internal-combustion haven for the foreseeable future.

However, for those countries with a stable, operational grid, how fast does power need to be delivered into the vehicles to satisfy customers? The 179 million chargeable vehicles forecast to operate by 2030 (143.5 million BEVs and 35.5 million plug-in hybrid electric vehicles) will have varying requirements.

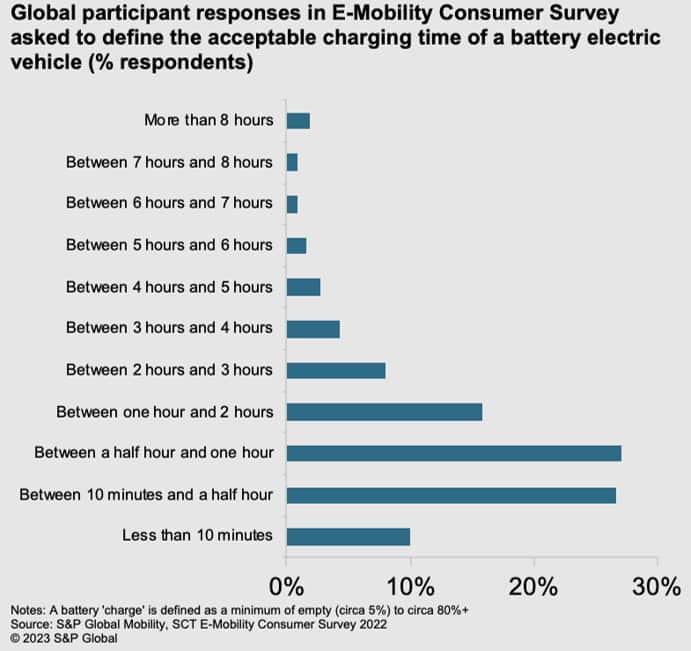

Grids cannot support fast charging everywhere all the time. In S&P Global Mobility's 2022 E-Mobility Consumer survey, the vast majority of global respondents contended that a charge time of between 10 minutes and two hours for a full charge (considered to be 80% by typical industry standards) would be acceptable. But nearly two-thirds wanted it to be performed in less than an hour.

BEV charging needs are situation-specific, with users needing the right speed of power delivery depending on their dwell time and journey profile. While BEV adopters to date predominantly charge at home, this will not be a workable solution for all.

Furthermore, for BEV charging providers, delivering a fast charge may not always serve their best interests. A burgeoning ecosystem is developing around the "30-minute retail economy" concept, which sees the opportunity to supply profitable services to users while they wait for public BEV charging. Such a retail ecosystem will provide charge point operators with a reason to scale, and help advances in charging technology if retail profits are reinvested.

With the evolution of EVs, charging technology will improve as higher-voltage architectures are adopted, bringing faster receipt of power. They will be enabled by the adoption of superior power semiconductor technology. Our data shows the volume of silicon carbide-based inverters will increase sixfold between 2023 and 2030 on their way to becoming the dominant inverter type by 2034.

A summary analysis of our latest forecast projections can be found in our EV Charging Infrastructure Report & Forecast.

Optimal range versus thermal management

Within the context of assessing charging infrastructure needs, the BEV's range dictates how often it needs to be charged and, potentially, where it will be charged. Critical here is a battery capacity of sufficient size to support range requirements. Less understood is the significant role of thermal management in getting a manufacturer's quoted all-electric range to reflect the "real world" range.

For BEVs on the market in 2023, the average all-electric range quoted is some 6.3 kilometers per kWh of battery capacity. S&P Global Mobility research estimates that some 28% of the range is lost using air conditioning throughout the drive cycle. As shown, this can be reduced to 15% using heat pump technology. Other than how the vehicle is driven, thermal management is the biggest parasitic loss for a BEV, save for an exceptional use case such as towing.

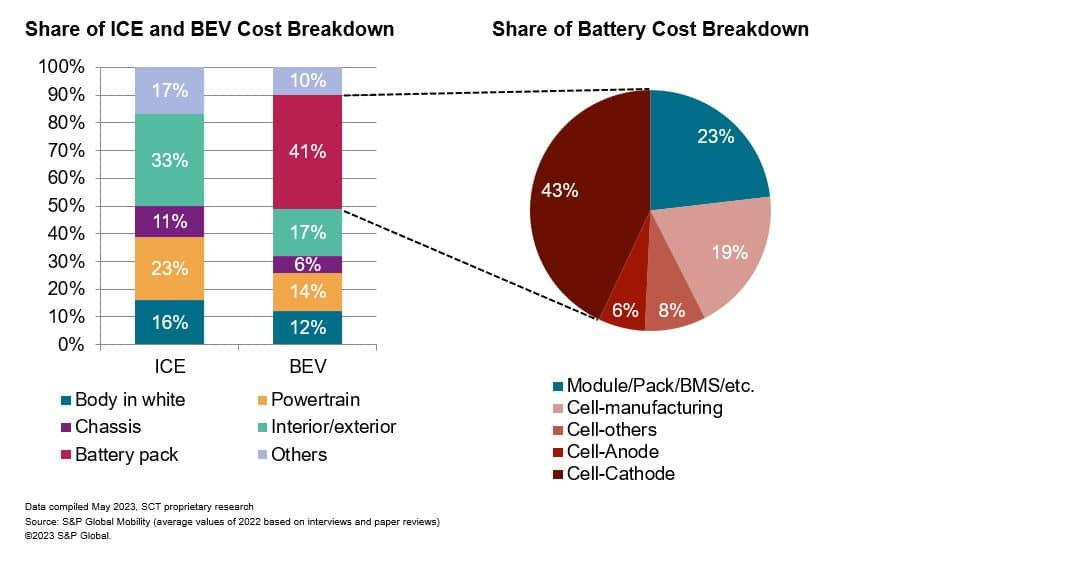

Heat pump technologies, integrated thermal modules (ITMs) and optimized battery preconditioning will also bring efficiency savings. While coolant-cooled battery solutions will become commonplace, niche enhancements in battery cooling technology, such as immersion cooling, will support in the short-term. As depicted below, thermal management of the BEV is a growth opportunity for suppliers with the monetary value contribution of thermal management to an electric vehicle increasing 83% compared with an ICE equivalent.

Currently, the thermal management system is a market of few players but presents a major opportunity. Continued consolidation in this domain through M&A to help suppliers build scale and countervailing the OEMs' power can be expected.

EVs for all? And profits for all?

This confluence of the above technological and logistical challenges triggers the need for BEVs to be available to as broad a customer base as the incumbent ICE technology. They must appeal for their key advantages and not be constrained by existing hindrances.

To ensure this, the cost of BEV technology must decline, and margins be sufficient for both OEMs and suppliers to thrive in a complex geopolitical environment. Recent research using S&P Global Ratings data showed that EBIT margins for OEMs are now consistently surpassing those of their suppliers — bucking historical trends. While multiple factors contribute, OEMs are squeezing suppliers to ensure sustainable profitability for their fledgling BEV businesses. Meanwhile, legacy OEMs and suppliers must manage the transition from ICE to BEV to ensure a stable glide path and not overextend.

The evolution of battery, charging, propulsion, and thermal management technology will be crucial for the ubiquitous adoption of BEVs. While scale inevitably helps, technological development is still required to make mass-market BEVs a product evolution inevitability rather than a subsidy-induced and government-mandated novelty.

--------------------------------------------------------------

Dive deeper into these mobility insights:

Electrification technology in reshaped supply chains for ubiquitous EVs

As the industry goes electric, expect a shakeout among internal combustion suppliers

Learn more about electric vehicle trends from our latest insights and solutions

The challenge of sourcing EV battery minerals in an ESG world