Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jun 04, 2024

Top five takeaways from May's global survey data as manufacturing PMI hits 22-month high

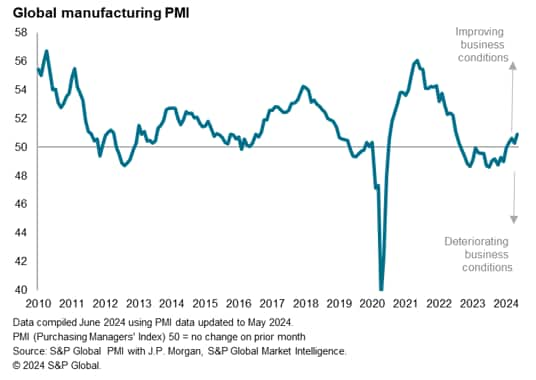

At 50.9, the Global Manufacturing PMI, sponsored by JPMorgan and compiled by S&P Global Market Intelligence, recorded above 50.0 neutral mark (and therefore in expansion territory) for a fourth straight month in April, the rate of growth gaining ground to the highest since July 2022. The latest data signalled an ongoing steady improvement of the global manufacturing economy so far in 2024 after almost one and a half years of decline.

The PMI is a composite index derived from five survey 'sub-indices'. Here are our top five takeaways from some of these sub-indices, as well as diving into the detailed anecdotal evidence provided by survey contributors, which provides a deeper insight into the current manufacturing trends relating to output, demand, inventories, supply chains, employment and prices.

1: Global output growth fastest since 2021 as upturn becomes more broad-based

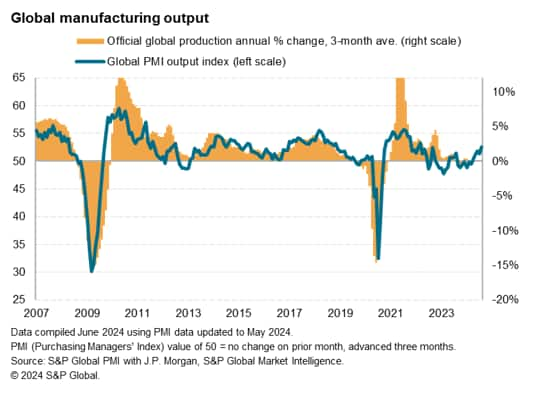

The PMI survey's sub-index of production, which tracks actual month-on-month factory output changes, signaled a fifth successive monthly expansion of production in May, with the rate of growth accelerating to the fastest since December 2021. The survey data are indicative of manufacturing output growing worldwide at an annual rate of approximately 2%.

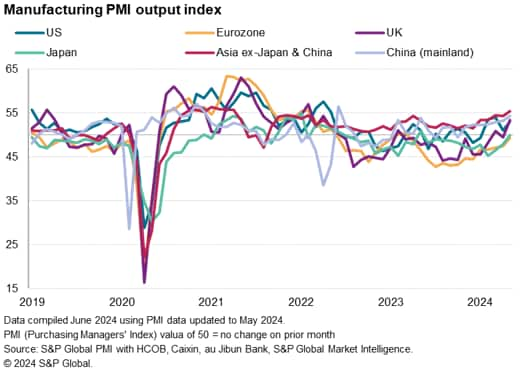

The production improvement was again led by Asia, but is becoming more broad-based. Excluding Japan and mainland China, Asia recorded the steepest expansion of output for just over three years, as sustained strong growth in India was accompanied by accelerating upturns in other economies in the region such as South Korea and Taiwan, where rates of growth hit 34- and 29-month highs respectively. However, growth also gained further momentum in mainland China to reach a 23-month high, and Japan saw output come close to stabilizing, recording only a marginal contraction that was the smallest seen over the past year.

The strengthening expansion in Asia was accompanied by a re-acceleration of growth in the US to the third fastest seen over the past two years, as well as a revival of production growth in the UK to the sharpest for 25 months. Eurozone manufacturing meanwhile registered the smallest contraction in the past 14 months.

2: Inventory building boosts global trade

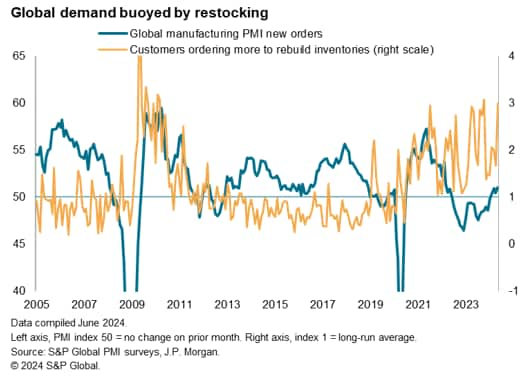

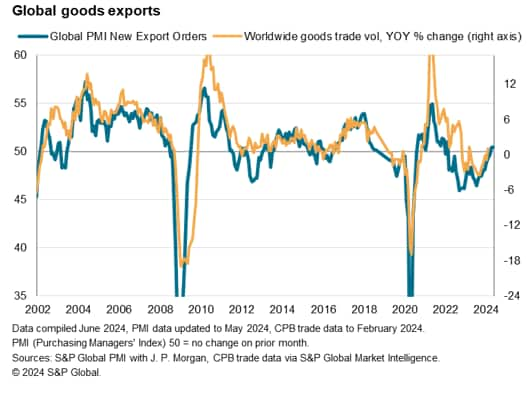

Global output growth was buoyed by new orders for goods rising at the fastest rate for 26 months in May. The improved demand environment in part reflected renewed stock building by customers, the incidence of which is now running at one of the highest seen since the initial recovery from the global financial crisis over a decade ago. Having depleted excess stocks, accumulated in the aftermath of the pandemic as demand switched from goods to services, companies are now rebuilding these inventory levels again in increasing numbers.

The demand upturn has in turn fed through to a revival of global goods trade, with the PMI signaling rising merchandise exports for a second consecutive month in May, ending an over two-year spell of falling global trade flows.

3: Supply chain stress remains low despite increased purchasing, for now

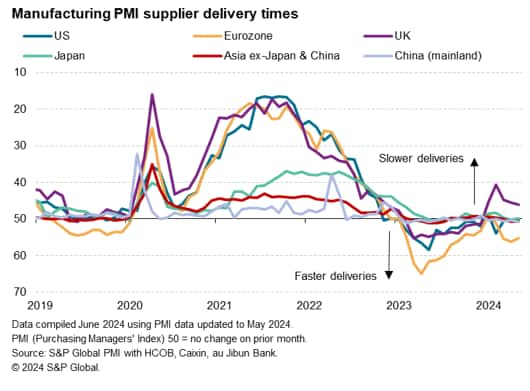

Although the amount of inputs purchased by manufacturers rose in May at a rate not seen in nearly two years amid restocking, global supply chains showed little sign of stress. Measured overall, global supplier delivery times improved marginally for the fourth successive month. The improvement marks a further contrast to the short-lived delays seen at the start of the year in response to the Red Sea shipping disruptions. As such, the PMI data point to both a limited and modest supply chain impact globally so far from the Red Sea issues. The upturn in purchasing nonetheless hints that, if sustained, we may see some lengthening of supply chains in the coming months based on past relationships between purchasing and supply chains.

The improvement in supply chains was by no means universal, however, with the UK once again a notable outlier among the major economies in seeing longer delivery times in May. An ongoing Red Sea impact was reported alongside Brexit-related import issues. The eurozone meanwhile reported a further noteworthy quickening of average delivery times.

4. Staff availability issues drive pay pressures

Although global employment rose marginally for the second time in three months in May, job gains were again subdued by difficulties finding or holding on to staff in many countries. The incidence of manufacturers reporting lower employment due to staff retention issues has been running at historically elevated levels in recent months, according to the PMI Comment Tracker data.

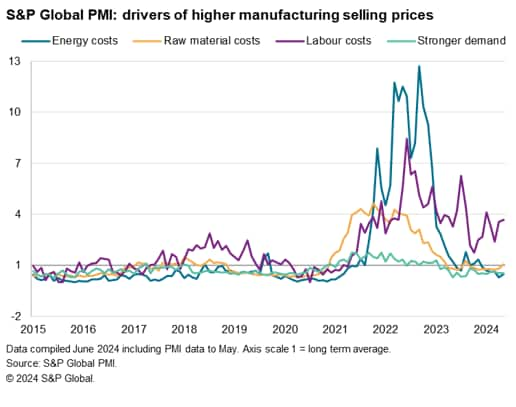

These tight labour market conditions continued to contribute to higher pay pressures. The PMI Comment Tracker data showed that upward pressure on factory selling prices from wages and salaries was reported to have been running at almost four times the long run average globally in May, having picked up again in the past two months.

While energy and demand-pull inflation forces remained below their long-run averages in May, upward pressure from raw material prices also rose above the long-run average (albeit modestly) for the first time since August, hinting at a rekindling of commodity price pressures.

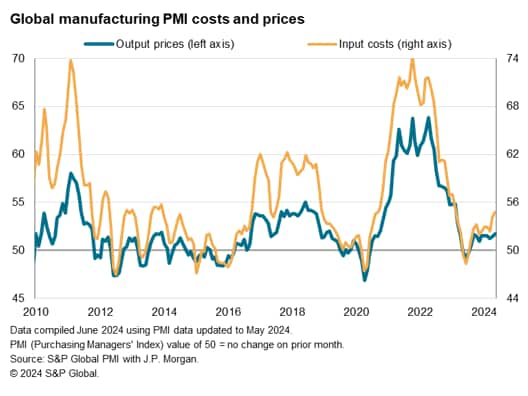

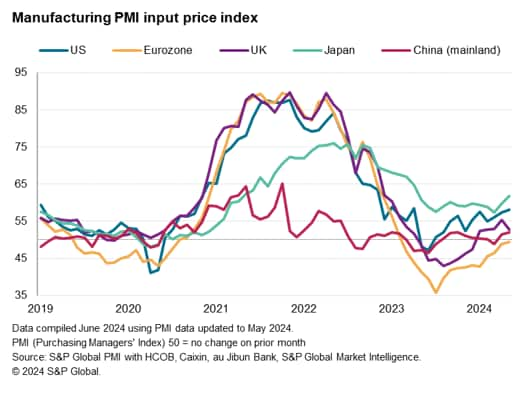

5: Manufacturing prices are adding to worldwide inflation

Measured overall, worldwide manufacturing input costs rose at the sharpest rate for 15 months in May. Although at 54.8 the global input cost index continues to run well below the pre-pandemic decade average of 55.6, the data suggest that rising costs are likely to exert some upward pressure on selling prices in the coming months, adding further to signs that the disinflationary spell from goods prices that has helped bring inflation down since the pandemic peaks is reversing. If supply chains lengthen amid rising input buying, some further upward pressure on prices may also be generated as pricing power shifts to suppliers.

Of the major economies, the steepest rate of input cost inflation was seen in Japan during May, where upward pressure on prices was exacerbated by the impact of the yen's recent weakness on import costs. However, US input cost inflation also accelerated to a strong rate, reaching a 13-month high and rising further above the pre-pandemic 10-year average.

The UK saw some moderation of price pressures due to the fading impact of the higher minimum wage (which was introduced in April). Meanwhile, the eurozone saw input cost fall, but the decline was the smallest seen for 15 months.

Input costs rose in mainland China at a rate not exceeded for nearly two years, helping drive costs up across Asia at the fastest rate for 15 months and adding to the evidence of an increasingly broad-based, recovery-led, firming of goods price inflation.

Access the Global Manufacturing PMI press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2024, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fqa.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2ftop-five-takeaways-from-mays-global-survey-data-as-manufacturing-pmi-hits-22month-high.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fqa.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2ftop-five-takeaways-from-mays-global-survey-data-as-manufacturing-pmi-hits-22month-high.html&text=Top+five+takeaways+from+May%27s+global+survey+data+as+manufacturing+PMI+hits+22-month+high+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fqa.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2ftop-five-takeaways-from-mays-global-survey-data-as-manufacturing-pmi-hits-22month-high.html","enabled":true},{"name":"email","url":"?subject=Top five takeaways from May's global survey data as manufacturing PMI hits 22-month high | S&P Global &body=http%3a%2f%2fqa.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2ftop-five-takeaways-from-mays-global-survey-data-as-manufacturing-pmi-hits-22month-high.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Top+five+takeaways+from+May%27s+global+survey+data+as+manufacturing+PMI+hits+22-month+high+%7c+S%26P+Global+ http%3a%2f%2fqa.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2ftop-five-takeaways-from-mays-global-survey-data-as-manufacturing-pmi-hits-22month-high.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}